If your middle credit score is already in the mid 700’s or more make sure to contact us about our Premium VIP Home Mortgage Lending Program, including Conventional, FHA, VA, and Jumbo options for borrowers who have what is considered excellent credit score … call to ask us about lower rates, faster closings and VIP service. Call 813-850-6021

Find out what really matters when it comes to credit and qualifying for a home mortgage loan. Give the mortgage credit experts a call from

Mon-Fri : 9:00 am to 5:00 pm

(all times Eastern)

813-850-6021

One of the questions I get every day from our callers is How do I increase my credit score so I can qualify for a home loan? Answer – get new credit (anyone can get a secured credit card) and keep it active but maintain a low balance the lower the better. Increasing limits and lowering balances on existing accounts will work too.

Most clients reply with “I have applied and no one will give me a new credit card or new credit account.” My typical answer is” find a credit union and open two secured credit cards. Try and get a $500+ limit, but anything is better that not replacing your older bad credit with positive new credit ”

- Most weight for your credit scores are from your last 24 months credit history.

- The top credit problem is no recent positive credit history. It’s also the easiest to solve. Get two secured credit cards from your local bank or credit union, in Tampa we recommend Wells Fargo or Suncoast Schools Credit Union.

- The most common mistake we see which can wreck someone’s credit score is paying off old collection accounts, Do not payoff old collection accounts. This can actually lower your credit score.

- If you are really interested in improving your credit score check out this ebook

. - While credit is not an important factor for a Hard Money or reverse mortgage equity loan, it is one of the most important parts of qualifying for an “A” credit (Conv., FHA,USDA, Jumbo) home loan.

We use Credit Xpert software on our credit reports which simulates potential credit scores after changes with great accuracy. We simulate paying down a credit card or increasing a credit limit. The software can predict what your score will be after the changes.

Why do we talk about using credit cards to improve credit scores so much?

Because they are easy to get or increase limits on and changes to scores can take effect quickly. Within 24-72 hours with Score Express or Rapid re-scoring. Reference: http://www.credittechnologies.com/Rescoring.asp

How can this benefit you in qualifying for a mortgage? Lets say your credit score was 20 points under the cutoff for the best mortgage program. In the past you would be told that you don’t qualify for program A (best rate, lower down) so you’ll have to accept program B (higher rate,more down) instead. Would it save you money if you could find out exactly how to get those extra points on your credit instantly? Now you can if your Florida mortgage broker is using Credit Xpert and Credit Radar technology.

Using another example let’s say your score was just 20-40 points below being able to qualify for a home loan at all. In this example you would be turned away altogether. This is not the case when using an experienced broker who is a credit expert for your mortgage loan.

Call us to get pre – qualified for a mortgage 813-850-6021

Please help support all of the time and effort invested in this case study, purchase this ebook![]()

from Amazon. You do not need a device you can read it online or on any device you choose.

I promise that if you take the time to read and follow the case study you’ll takeaway something and learn how to improve your score without spending any money on credit repair.

Companies that help improve your credit score may use shady tactics such as writing mass letters to the credit agencies in hopes they do not respond within 30 days. This could force the credit bureau to remove the item from your report even if it’s really your negative item. This could work temporarily but the creditors end up re-reporting the accurate info and it can go back on your file. The chances of getting items that are accurate and truly belong to you removed from all three bureaus is slim to none.

Don’t get scammed with credit repair. Check out this FTC article before you sign up for expensive credit repair.

reference: http://www.ftc.gov/bcp/edu/pubs/consumer/credit/cre13.shtm

How to Boost Credit Score Case Study

I have so many people call and tell me their story when trying to qualify for a home purchase with credit issues I thought I would walk you through a real life case study of a client that was nice enough to allow me to share screenshots and every detail about his credit situation. Follow along our instruction and guided path to re-establishing credit.

John is a married guy with a wife and three kids. When he lost about 50% of his income he had no choice but to default on a several loans and credit cards in order to keep a roof over their heads. John has not applied for or used any credit since these defaults happened over two years ago. Some of the defaults have turned into judgement(s) due to creditors filing a court case to collect on the defaulted debts. John will likely have to settle those after fixing his scores and establishing new credit before he can get a conventional or government mortgage. He could however get new car loans, portfolio or a private mortgage without settling the judgement(s).

How do I get my credit score for free online?

Using these two free website services: (1) CreditKarma.com to get TransUnion scores and (2)CreditSesame.com to get Experian credit data he has agreed to share step by step how he is going about improving his credit following our plan and advice.

Step One: Go to each website and setup and account to get a current score.

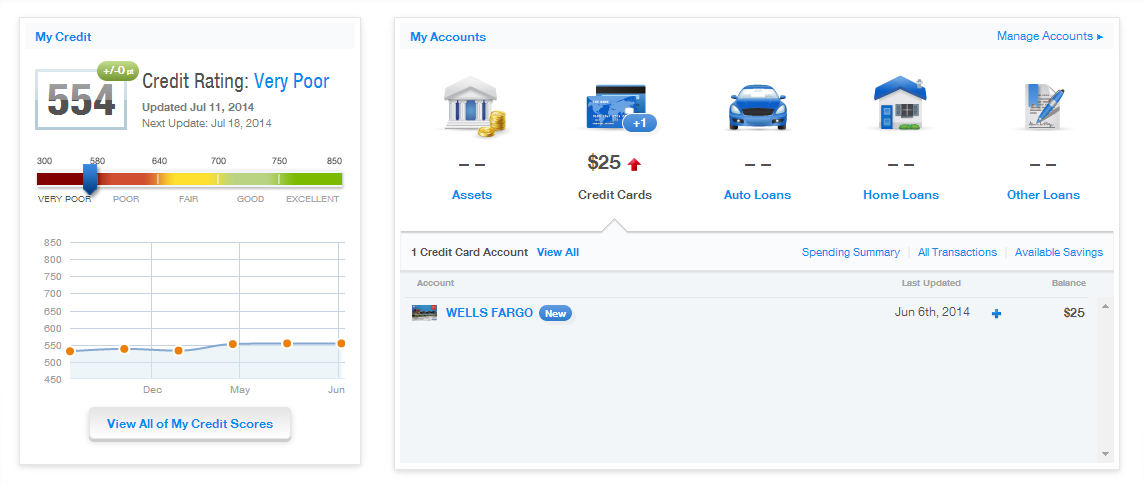

John’s starting scores were 533 TransUnion and 640 Experian. For home lending we always use the lower of two or middle of three. So for qualifying purposes he a 533, only good enough for a private mortgage and maybe a bank portfolio loan with a large 40% down payment.

How to raise your credit score with a credit card

Step Two: Get new credit, secured credit cards. Our standard advice is two cards since lenders are looking for 12 months good history on two or three accounts. Your current rent or mortgage cancelled checks can be counted as the 3rd reference.

John applied for and received one $500 limit secured credit card that his bank, Wells Fargo offered through their online banking website. He has been using it since he got it in late May and his low score has increased to the 552-554 range.

This screenshot shows the New Wells Fargo secured credit card that was opened in May.

His TU score went up almost 20 points to 552 just before the new card showed up on the reports. The EXP score is at 639 now in September.

Using the Credit Karma credit score simulator John can see that adding a 2nd credit card with a $500 limit will increase the score to 588. Increasing his current secured Wells Fargo Visa card by $500 could increase the score to 571 without adding a 2nd card.

If you already have credit cards increasing the limits (available credit) can give you a boost

By taking our advice and getting two secured cards John can get his score a little higher than just one with a larger limit according to the credit score simulator.

Adding a new credit card with a $500 limit will increase the score to 588 from 552. That’s another 34 points from the original 533.

I want to stop and take a minute to explain more about how these websites are able to provide your score information for free. They display offers for loans and credit advertising on their website. If you choose to apply for these offers they are compensated by the lenders. It’s a great strategy. Provide an excellent service for free and get paid with advertising or if visitors decide to use the advertised services.

How to get a copy of your credit report

You can also get detailed reports from the government authorized website https://www.annualcreditreport.com/index.action at no charge once per year and more often is some circumstances like if you are denied credit or employment. You will have to pay for the scores since the government does not require the credit agencies to provide them with your annual report. This is why I recommend using the non government sites mentioned above as well to track your progress and get access to the score simulator tool.

We’ll update this case study with John’s progress each month.

September Update

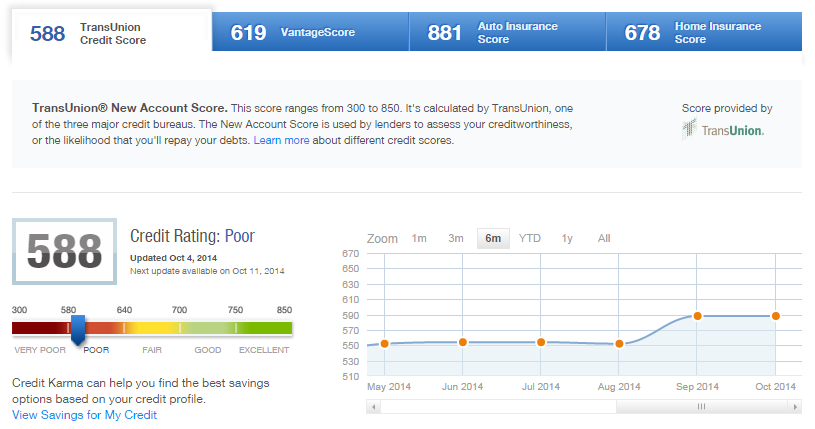

Your creditors report new information about your accounts and payment history on or around the 6th of each month. We just checked John’s account and his TU jumped to 563 for September. Here are the screenshots. So far with three months of payment history and one secured card he has gone from 533 to 563. The Experian is at 639 when checked on Credit Seasame.

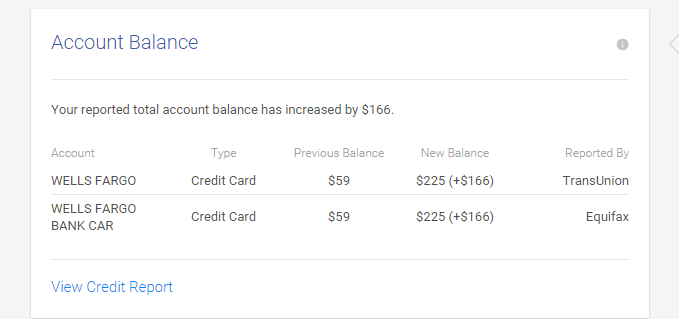

You can see the last two months John’s credit card balance has been more than 30% of it’s 500 limit when reported to the bureau. We are going to ask him to make payments anytime it goes above $100 to keep the utilization down below 20%. I suspect this could pit his score over 580 within the next two months.

You can see here that even with over $20,000 in collections, judgement and repossessions is is possible to improve.

September improvements

![]()

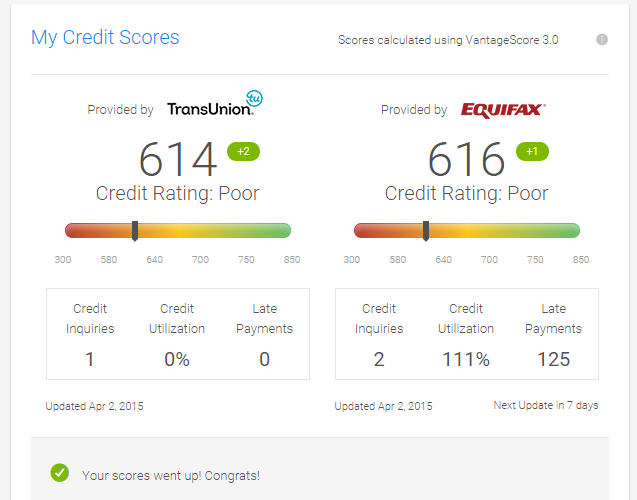

October Update

Our case study subject “John” increased his score to 588!. That’s good enough for a Specialty FHA home loan and Portfolio lending as well. Even though John does not have any urgent plans to finance a home he is happy to know he could based on this new rating. This month he made a a payment every time his $500 limit secured credit card exceeded a $100 balance and they reported a $133 balance of the $500 limit to the credit agencies. This lower credit utilization along with another on-time payment brought us the desired results. The score increased over that key 580 benchmark. If this were a letter grade system John went from an F to a D this month.

Our ultimate goal for this case study in to get John’s score above 640 so we’ll continue to check in on his Transunion score via the Credit Karma account until it reaches at least to our 640 goal.

- Our advice to get to reach the next goal.

- Get that 2nd secured or unsecured major credit card.

- Keep the balances very low with unused available credit high

- Continue to make on time payments on all accounts. Just one late payment could put John back down in the 530’s. Plus mortgage lenders need to see 12 to 24 months with no 30 day late payments.

- Only apply for one more account right now. Lots of credit inquires are bad and can reduce the score.

Here is the screenshot

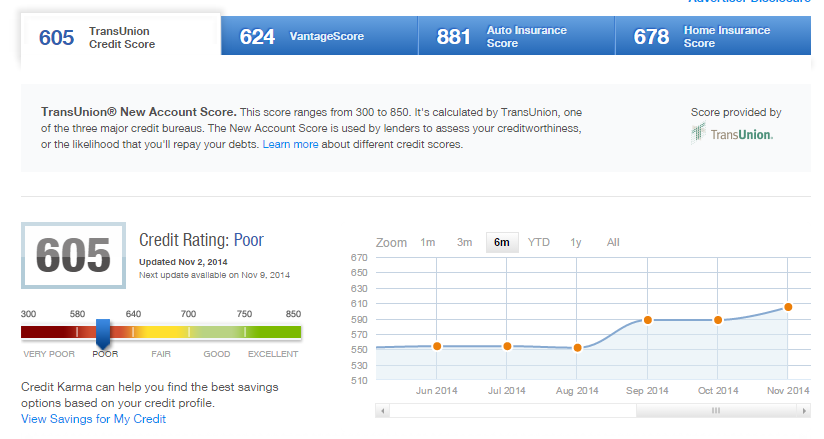

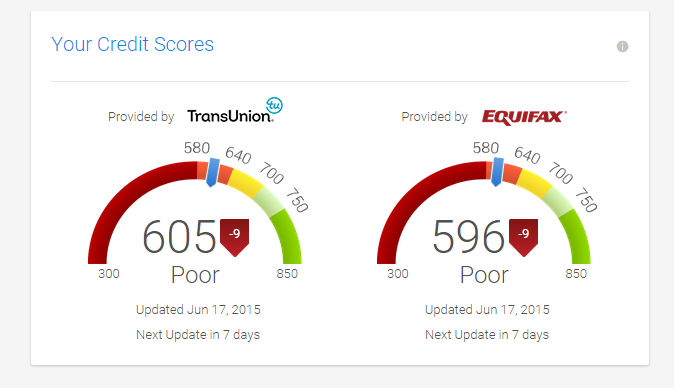

November update. Our case study subject’s Transunion score came in at 605 this month!  He still has not applied for the second secured credit card. He is probably waiting to get a decent unsecured card for his next tradeline (account). We always recommend two or three accounts because this is what home lenders like to see when considering an application for approval.

He still has not applied for the second secured credit card. He is probably waiting to get a decent unsecured card for his next tradeline (account). We always recommend two or three accounts because this is what home lenders like to see when considering an application for approval.

If you are motivated to re establish credit in order to purchase a home make sure you get two or three accounts in order to establish that 6-12 month one time payment history. As you can see if you keep the balances very low and never above 30% of the limits your score will rise quickly after a few months of low balances reported with no 30 day late payments. If you already have revolving accounts with high balances simply lower the balances and or increase the limits to improve your credit rating quickly.

If you have made in this far and followed all of the steps shown in our case study example you likely have or now know how easy is is to get a 640 credit score using secured or unsecured credit cards.

Go from 640 to 740 by paying off credit card debt with an installment loan.

Some of you that are carrying lots of credit card debt and cannot get past that 640-660 mark may want to consider an unsecured consolidation loan from a high qualify P2P lender (person to person lender). Click on the banner below to bring your credit card balances down and take your score to the next level. Remember paying off revolving credit balances with a fixed installment loan can be worth 75 to 150 points. You can easily exceed the 700 – 740 mark by paying off balances with an installment loan. Click on the banner and you’ll get an approval in about 5 minutes, if you are 640 or above you can get between $2,000 to $35,000 with an unsecured fixed installment P2P loan.

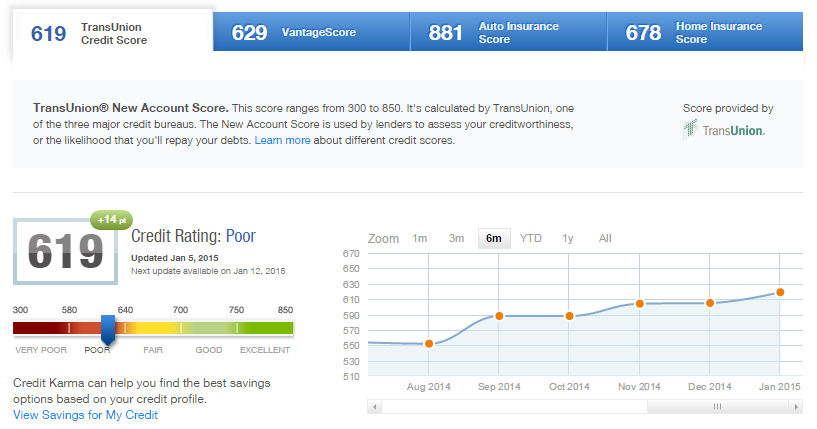

Update: January 5, 2015

Here is our January Credit Score Improvement Case Study Results Report

Our volunteer’s score updated today to a 619.

If you skipped down to this point in our case study I’ll bring you up to date. “John” had many defaults that were a few years old and has been paying cash ever since his loss of income contributed to him defaulting on several accounts between 2009 and 2011. These accounts ended up in charge off, collection and judgment statuses.

He has not settled or paid off any of these accounts. He did not use any credit repair tactics to remove attempt to remove them from his report.

- He simply took our advice and got a secured visa credit card from his local Bank, Wells Fargo, for $500.

- He does not put more than $100 on the card before paying off the balance each month.

- He has made the payments on-time each month.

We also suggested he get a 2nd credit card and do the same thing to speed the score increase up based on simulation results of adding a 2nd card with a $500 or greater limit. He has not done this yet maybe by next month he’ll get this done.

Today we checked his his Credit Karma account and he is now up to 619 Transunion (his lowest bureau). 620 is the point where many major lenders will issue a mortgage with a low down payment. By opening just one secured credit card, keeping the balance low, and making all of the payments on time for about 6 months he has been able to get workable credit in a short period of time.

Here is this month’s screenshot from CK.

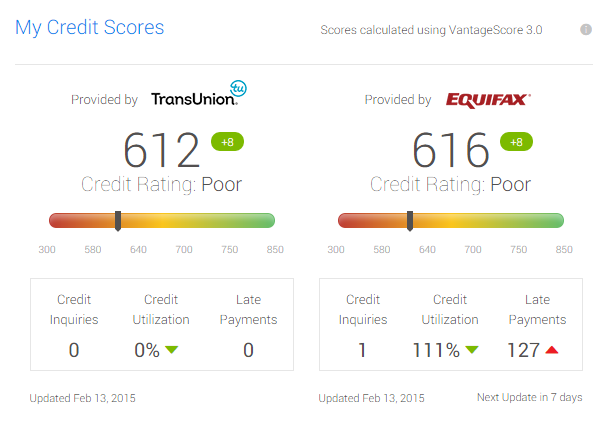

February Score Update

It’s February already and our case study subject’s scores are holding in the low 600’s, with the mid at 616. John’s scores will jump above 640 quickly if he get’s another credit card with a $500 limit. He says he is going to apply for a Capital One unsecured or try for an unsecured card at his bank to add a 2nd card increasing his available unused credit limits.

Credit Karma has redesigned their dashboard and added Equifax credit data to their customers’ accounts. So now you get to see TransUnion and Equifax side by side on their website. Quizzle also gives you Equifax data. For the third score we are using Credit Sesame which provides Experian data. Our volunteer John is at a 636 Experian.

See the graphic below for the other two.

See two scores, Equifax and Transunion side by side now on CreditKarma

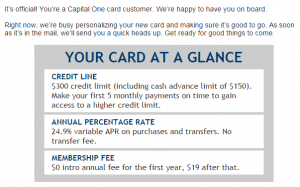

March Update “Good News From Wells Fargo”

Our credit guinea pig contacted us with some big news. He applied for a Capital One unsecured credit card and was instantly approved online for a starting credit limit of $300. There is no security account required for this account which is what John wanted for his 2nd card.

The funny thing is the same day he noticed an inquiry from Wells Fargo on his report. Then he got the “good news letter” that his security deposit was being returned on the WF account and effective in April he will get a big upgrade in benefits and terms on his first card.

The card upgrade contains the following improvements

- $0 Annual Fee – It was $25 for before the upgrade

- A Lower variable APR of 15.65% on purchases

- A return of collateral deposit

John has made great progress by taking things slow and now he has two unsecured accounts. With continued low balances and on time payments his rating will keep rising. He is ready for FHA or non-prime home loans. He could get a reasonable auto loan with his newly improved credit rating.

You can do it too! Start by saving for a deposit on a good secured card then applying for the Capital One Platinum card for average credit. You can do this much faster and you will likely see a quick 20-100 point jump depending on where you are starting from.

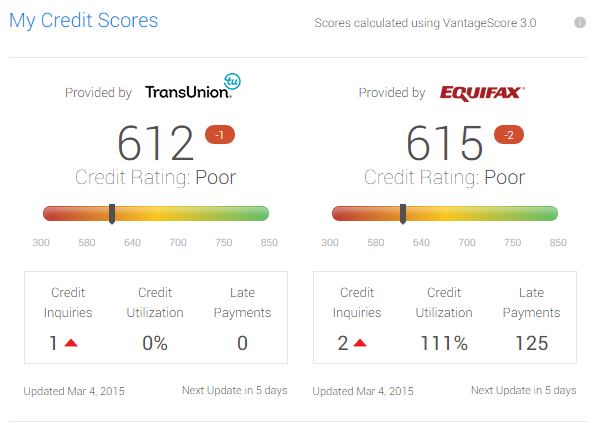

April Case Study Update

It’s that time again, time to check for beginning of the month score updates on our case study. We mentioned there was a 2nd credit card added. A Capital One unsecured starter card with a $300 limit. It has a $25 annual fee with is waived for the first year. They promised to raise the limit to $500 if the card is used and paid on time for the first five months.

Below is the screenshot from Credit Karma showing TransUnion at 614 and Equifax at 616. Credit Sesame switched their credit provider to Trans Union so we lost Experian data until we find another free provider who uses them. Last time we were able to check that one was 636 and it has not changed throughout this case study. Credit repositories are regional here in Florida most creditors report mainly to EFX and TU.

June Update

Scores drop with sudden increase in credit card balances

It’s been over a year since our case study started and the highest we have seen is 619 which is 39 points above the minimum score for a low down payment home loan. We have been able to help him bring his scores up over 79 points from the 540 range when we started.

Our goal is 640 which will take some time for the credit limits to increase and the new accounts to age along with the good payment history.

Our case study subject still has some large $17,000~credit card collections reporting as if they were open and active accounts over their limits in his Equifax bureau.

Below are this months screenshots showing a 9 point decrease due to the sudden increase in credit card statement ending balance. This was paid off before the due date but the creditors report the statement ending balance each month. The only way to avoid this is to put less on the cards or to make extra mid month payments any time the balance goes over $50.

Feel free to ask questions or give us your own update if you are following along in the comments section below this guide.

Credit score chart 2015 for loans and credit grades

Here is the range lenders use as a rating scale to approve and price out borrowers loans for mortgages, cars, personal loans etc.

AAA 740 to 801+ This range is considered excellent and lenders will offer the best rates – approve for the best loan programs

AA 720-739 Just below the excellent category these scores will have a slight increase in rates and fees. If you fall into this category you can still get approved for most loans.

A+ 700-719

A- 680 – 699

B 660 – 679 The A minus grade will get you approved for most programs with about a .25% increase in rates and or a 1.25% to 3% increase in discount point fees.

B- 640 – 659 This credit grade will have a substantial price increase in rate and discount fees. It’s also the lowest lending category that many banks and lenders will consider. Scores lower than this will usually require using a sub-prime, non-prime or specialty lender.

C 620 – 639 This is the minimum range required to get a conventional loan. Anything lower will need to go FHA or with a specialty lender that will hold the loan in their portfolio.

C- 580 – 619 Here your options get very limited to specialty or portfolio lending. Lenders may require a manual underwriting process and make you jump through more hoops.

D 550-579 Believe it or not you can get home loan even with a score this low. Specialty lenders will require 10% or more as a down payment. Or in the case of a refinance more equity ( lower loan-to-value) will be required.

550 and below. Borrowers in this range will usually need a private or portfolio lender who will require 40 to 50% as a down payment. Financing becomes very niche and local with private lenders in this range.